Tax planning and strategizing should occur all year long, not just at year-end. We understand the many rules and regulations governing the tax landscape and can help you to determine the best solutions for your business.

Our tax team is knowledgeable about the numerous tax issues that face businesses and can help with business structuring, business tax planning, business tax credits, multistate/Nexus planning, and much more. Contact SVA today for all of your business tax needs.

Business professionals need easy access to information to make timely decisions. SVA has what you need, when you need it. Choose a topic below or just contact us directly. Our expertise is ready anytime you need it.

This eguide covers different tax credits and deductions available to businesses, as well as what to look for in a tax advisor, choosing a tax-advantaged business entity and more!

Visit SVA’s Web Tax Guide to access a wide array of resources that can help prepare you and your business for the upcoming tax season.

Download the 2026 Federal Tax Rates PDF to get all the 2026 tax rates.

Keeping your tax liability to a minimum is key to your overall financial health. This guide contains tax-reduction strategies for individuals and businesses.

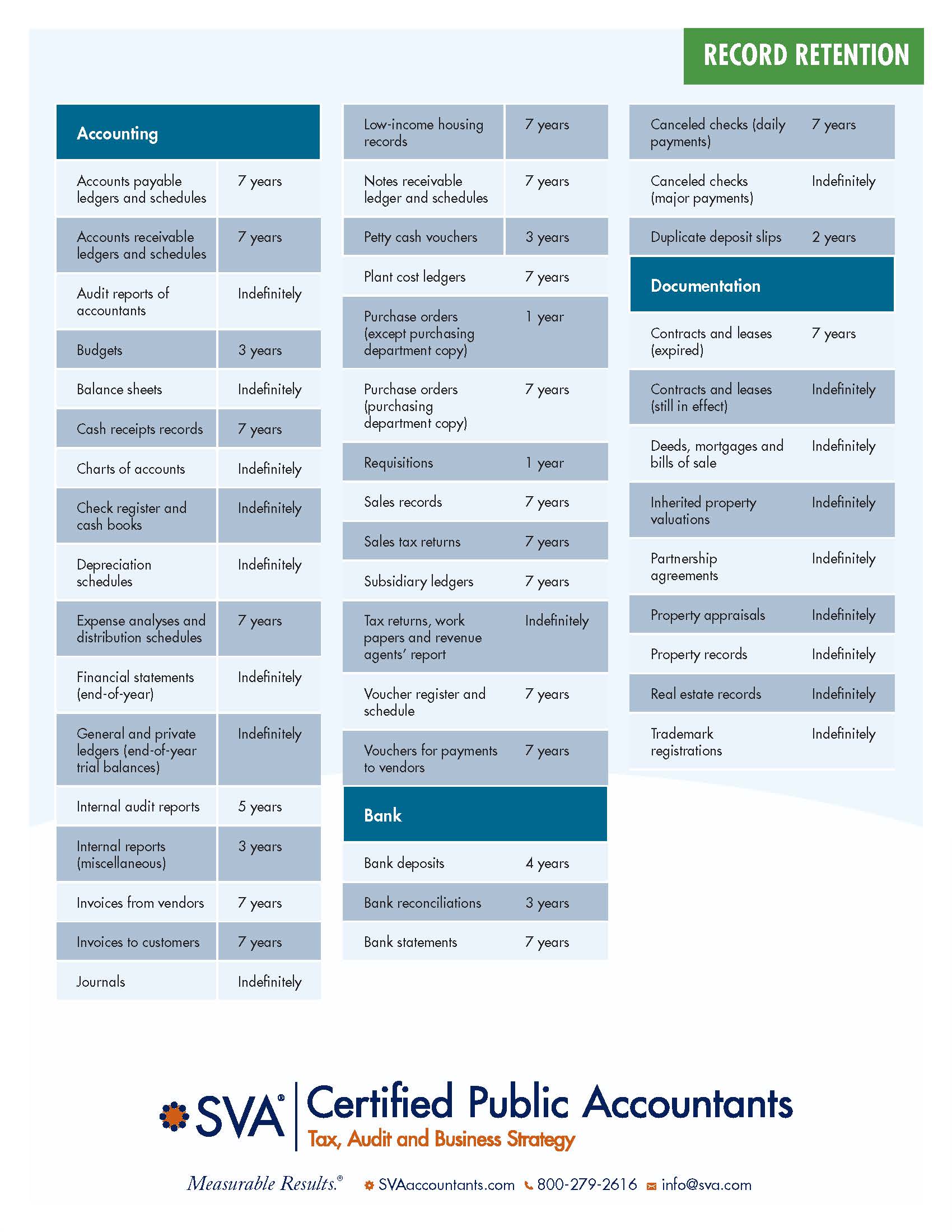

Not sure how long to keep certain records for your business? Download this guide to help you keep track.

Madison, WI

1221 John Q Hammons Dr, Suite 100

Madison, WI 53717

(608) 831-8181

Milwaukee, WI

18650 W. Corporate Drive, Suite 200

Brookfield, WI 53045

(262) 641-6888

Colorado Springs, CO

10855 Hidden Pool Heights, Suite 340

Colorado Springs, CO 80908

(719) 413-5551

Copyright © 2026 SVA Certified Public Accountants | Privacy Policy | Cookie Policy | CCPA

{kind=link}