Scroll down to continue reading.⬇

Tax regulations are created and modified by legislation passed by Congress. As we discuss the various tax regulations and opportunities, several bills will be referenced as these significantly impacted the tax opportunities available to individuals and business owners.

To help guide you through the acronyms, here is a quick list of the legislation:

| OBBBA | The One Big Beautiful Bill Act was a comprehensive piece of legislation that brought together multiple provisions across tax, spending, and regulatory policy. It aims to streamline complex rules, expand opportunities for individuals and businesses, and address wide-ranging national priorities in a single package. |

| TCJA | The Tax Cuts and Jobs Act changed deductions, depreciation, expensing, tax credits, and other tax items that affect businesses. |

| IIJA | The Infrastructure Investment and Jobs Act created a modest number of tax changes and focused on spending for roads, highways, bridges, public transit, and utilities. |

| IRA | The Inflation Reduction Act included significant provisions related to climate change, health care, and taxes. |

A tax credit is considered more favorable than a tax deduction because it reduces the tax due, not just the amount of taxable income.

A tax deduction reduces your taxable income and the tax rate used to calculate your taxes. The result can be a larger refund of your tax withholding.

A tax credit reduces your taxes which gives you a larger refund of your withholding. Plus certain tax credits can give you a refund even if you have no withholding.

Here is an Example of the Impact of a $10,000 Tax Deduction vs. a $10,000 Tax Credit:

| Tax Deduction | Tax Credit | |

| Adjusted Gross Income | $90,000 | $90,000 |

| Less Tax Deduction | ($10,000) | |

| Taxable Income | $80,000 | $90,000 |

| Tax Rate Example | 25% | 25% |

| Calculated Tax | $20,000 | $22,500 |

| Less Tax Credit | ($10,000) | |

| Your Tax Bill | $20,000 | $12,500 |

Projecting your business’s income for this year and next can allow you to time income and deductions to your advantage. It’s generally — but not always — better to defer tax.

If your business uses the cash method of accounting, you can defer billing for products or services at year-end. If you use the accrual method, you can delay shipping products or delivering services.

If you’re a cash-basis taxpayer, you may pay business expenses by December 31st so you can deduct them this year rather than next. Both cash and accrual-basis taxpayers can charge expenses on a credit card and deduct them in the year charged, regardless of when the credit card bill is paid.

If your business is a flow-through entity and you’ll likely be in a higher tax bracket next year, accelerating income and deferring deductible expenses may save you more tax over the two-year period.

An organization that is formed for one or more people to conduct business activities is known as a business entity.

The choice of business entity structure is crucial as it determines how the entity is taxed and who will be liable for paying the obligations and debts.

Income taxation and owner liability are the main factors that differentiate one business entity structure from another.

Many businesses choose entities that combine pass-through taxation with limited liability, namely limited liability companies (LLCs) and S corporations. But recent changes warrant revisiting the tax consequences of business entity structures.

The flat corporate tax rate is significantly lower than the top individual rate, providing significant tax benefits to C corporations and helping to mitigate the impact of double taxation for owners.

In addition, the corporate alternative minimum tax (AMT) has been repealed, while the individual AMT remains (though it will affect far fewer taxpayers). But the TCJA also introduced a powerful deduction for owners of pass-through entities.

For tax or other reasons, a structure change may be beneficial in certain situations. But there also may be unwelcome tax consequences that effectively prevent such a change.

| Entity Type | Ownership | Personal Liability of Owners | Tax Treatment |

| C Corporation | Unlimited number of shareholders allowed; no limit on stock classes | Generally no personal liability of the shareholders for the obligations of the corporation | Corporation taxed on its earnings at the corporate level and the shareholders have a further tax on any dividends distributed (double taxation) |

| S Corporation | Up to 75 shareholders allowed; only one basic class of stock allowed | Generally no personal liability of the shareholders for the obligations of the corporation | Entity generally not taxed as the profits and losses are passed through to the shareholders (pass-through taxation) |

| Sole Proprietorship | One owner | Unlimited personal liability for the obligations of the business | Entity not taxed as the profits and losses are passed through to the sole proprietor |

| General Partnership | Unlimited number of general partners allowed | Unlimited personal liability of the general partners for the obligations of the business | Entity not taxed as the profits and losses are passed through to the general partners |

| Limited Partnership (LP) | Unlimited number of general and limited partners allowed | Unlimited personal liability of the general partners for the obligations of the business; limited partners generally have no personal liability |

Entity not taxed as the profits and losses are passed through to the general and limited partners |

| Limited Liability Company (LLC) | Unlimited number of members allowed | Generally no personal liability of the members for the obligations of the business | Entity not taxed (unless chosen to be taxed) as the profits and losses are passed through to the members |

Measurable Results.® SVA's Tax Plan Strategy Expertise Benefits Barnes, Inc.

Measurable Results.® SVA's Tax Plan Strategy Expertise Benefits Barnes, Inc.

Made permanent with the One Big, Beautiful Bill Act (OBBBA), the Section 199A deduction is for sole proprietorships and owners of pass-through business entities such as partnerships, S corporations, and LLCs that are treated as sole proprietorships, partnerships, or S corporations for tax purposes.

Qualified Business Income (QBI) is the net amount of qualified items of income, gain, deduction, and loss from any qualified trade or business which includes income from partnerships, S corporations, sole proprietorships, and certain trusts.

The QBI deduction generally equals up to 20% of qualified business income (QBI), but it is subject to limitations that apply when taxable income exceeds certain thresholds. These thresholds are adjusted annually for inflation and vary based on filing status.

For taxable income above the threshold, a special formula is used to calculate the deduction, incorporating factors such as wages paid by the business and the unadjusted basis of qualified property.

To determine your specific eligibility and deduction amount, consult the latest IRS guidelines or speak with a tax professional to ensure compliance with current regulations.

Taxpayers sometimes confuse bonus depreciation with Section 179 expensing. The two tax breaks are similar but distinct.

1. Like bonus depreciation, Section 179 allows taxpayers to deduct up to 100% of the purchase price of new and used eligible assets in the year they are placed in service. Eligible assets typically include software, computer and office equipment, certain vehicles and machinery, and qualified improvement property. However, Section 179 is subject to certain limits that do not apply to bonus depreciation. These limits, such as the maximum allowable deduction and phase-out thresholds, are adjusted annually for inflation. Taxpayers should consult the latest IRS guidelines or a tax professional to determine the current deduction limits and ensure they maximize their benefits under Section 179.

2. In addition, the Section 179 deduction is designed to benefit small- and medium-sized businesses, so it begins to phase out on a dollar-for-dollar basis once total qualifying property purchases exceed a specified threshold. If the total cost of Section 179 property placed in service during the year surpasses this limit, the deduction may no longer be available. Both the maximum deduction amount and the phase-out threshold are adjusted annually for inflation. To determine the current limits and ensure compliance, taxpayers should consult the latest IRS guidelines or a qualified tax professional.

3. The Section 179 deduction also is limited by the amount of a business's taxable income, applying the deduction can't create a loss for the company. Any cost not deductible in the first year can be carried over to the next year for an unlimited number of years. Such carried-over costs must be deducted in chronological order, with older costs being deducted before newer ones.

4. Alternatively, the business can claim the excess amount as bonus depreciation in the year the property is placed in service. For instance, if you purchase machinery that costs $20,000 but have only $15,000 in income available for a Section 179 deduction, you can deduct $15,000 under Section 179, and the remaining $5,000 may qualify for bonus depreciation, subject to the applicable percentage.

5. Also, in contrast to bonus depreciation, the Section 179 deduction isn't automatic. You must claim it on a property-by-property basis.

It’s probably no surprise that businesses in many industries across the U.S. undertake innovative work every day.

From designing new products and processes to testing prototypes, improving current products and processes, engaging in testing and certifying and more, innovation drives growth — and growth plays a vital role in today’s competitive business landscape.

What may surprise you is that those businesses, including potentially yours, have an opportunity to receive substantial money for their innovative work. Thanks to federal and state research and development (R&D) tax credits, this opportunity exists.

Today, R&D tax credits are one of the most significant tax tools under current law for maximizing a business’s cash flow.

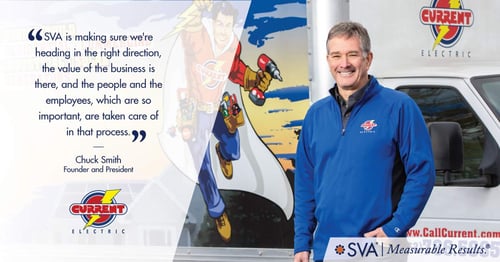

Measurable Results.® SVA Helps Current Electric with Year-End Tax Planning and Succession Planning

Measurable Results.® SVA Helps Current Electric with Year-End Tax Planning and Succession Planning

In fact, according to industry experts, less than 33% of companies that qualify for R&D credits apply for them. Consequently, millions of dollars undoubtedly go unclaimed each year. Why is that?

The chief reason lies with a long-held misconception, still prevalent today, that R&D tax credits are reserved for companies with established R&D departments staffed by “white lab coat” types (e.g., scientists, medical researchers, technicians, and testing personnel). The misconception was further entrenched by the temporary nature of the tax credit program over many years (specifically, it was hastily extended more than a dozen times since its passage in 1981).

Thankfully, federal R&D tax credits have now been made permanent, so there is no better time to reinvest in your business by getting credit for your qualified R&D activities.

While lots of businesses in many industries potentially qualify for R&D tax credits, “typical” R&D businesses (e.g., professional, scientific, and technical services) comprise only 10% of all credits claimed, according to the IRS.

On top of that, only one out of every 20 eligible businesses takes advantage of the R&D credit. Why?

Because many companies don’t realize that their industry is ripe with eligible activities. So, which of your business’s activities could potentially qualify? An R&D tax credit survey can help you make that determination.

In general, if your company has invested money, time, and resources in activities that help improve a process, product, technique, or formula, or contribute to the invention of a new process or product, you stand a good chance of qualifying.

Additionally, certain expenses qualify for R&D tax credits. These include supplies directly linked to qualified research activities, wages related to performing a qualified service, and payments to third-party contractors that meet the same qualification requirements for wages.

Now that you have a better sense of the R&D tax credit, what kinds of activities potentially qualify, and in what industries such activities typically occur, how do you know if your activities are eligible for R&D tax credits?

The R&D tax credit incentivizes certain research activities by reducing a company’s liabilities for spending money on that research. The credit is equal to a certain percentage of a business’s qualified research expense (QRE) over a base amount.

Expenses that qualify are more comprehensive than you may think — QREs can include the salaries of employees and supervisors conducting research, supplies, and even some of the research contracted out.

Regardless of your business’s size, revenue, or industry, the IRS’s Four-Part Test can help you determine whether your work meets the R&D tax credit eligibility.

Even though the R&D tax credit is a lucrative incentive by most standards, it has proven to be an elusive target for many businesses. That’s largely because confusion over qualification and documentation has prompted far too many companies to turn away from the credits, leaving them primarily within the sphere of large companies and the high-tech industry.

For this reason, we recommend that business owners partner with an outside expert to manage the nuts and bolts of an R&D tax credit survey for their company.

An R&D tax credit survey from a professional R&D tax expert will help you determine which of your business activities qualify and they will guide you through the documentation needed for eligibility.

Eligibility requirements are clearly defined by the IRS and governments in states that offer R&D tax credits. Any company considering the R&D tax credit path should be prepared to identify, document, and support its qualifying activities.

In this regard, it is critical to establish appropriate tracking mechanisms and documentation strategies for all R&D activities.

Operating in another state means possibly being subject to taxation in that state. The resulting liability can, in some cases, inhibit profitability. But sometimes, it can produce tax savings. Nexus means a business presence in a given state that’s substantial enough to trigger that state’s tax rules and obligations. Precisely what activates nexus in a given state depends on that state’s chosen criteria.

Even limited in-state service visits are a physical-presence trigger and can create sales/use and income/franchise tax nexus. Don't assume "a few calls" is below the radar.

If your company already operates in another state and you’re unsure of your tax liabilities there, or if you’re considering starting up operations in another state, consider conducting a nexus study. This is a systematic approach to identifying the out-of-state taxes your business activities may expose you to.

Keep in mind that the results of a nexus study may not be negative. You might find that your company’s overall tax liability is lower in a neighboring state. In such cases, it may be advantageous to create nexus in that state (if you don’t already have it) by setting up a small office there. If all goes well, you may be able to allocate some income to that state and lower your tax bill.

Tax planning is an essential part of your business strategy. Each business has its own unique circumstances and using an experienced tax advisor who will delve into your specific situation is imperative.

This eGuide provides highlights of each tax credit and deduction currently available. But rules shift and change and understanding how to use each option together will net the best results. Tax planning is a year-round discussion. Don’t wait until year-end.

SVA's 2025 - 2026 Tax Planning Guide

Madison, WI

1221 John Q Hammons Dr, Suite 100

Madison, WI 53717

(608) 831-8181

Milwaukee, WI

18650 W. Corporate Drive, Suite 200

Brookfield, WI 53045

(262) 641-6888

Colorado Springs, CO

10855 Hidden Pool Heights, Suite 340

Colorado Springs, CO 80908

(719) 413-5551

Copyright © 2026 SVA Certified Public Accountants | Privacy Policy | Cookie Policy | CCPA